What is the tax-free allowance?

The tax-free allowance is the amount of Gross Income you can earn in a year without having to pay any tax. The tax-free amount is set every year in the budget and is announced by the Chancellor.

What is the allowance for the year 6th April 2020 to 5th April 2021?

There are 3 main incomes where tax-free amounts can be earned:

- General income and wages: £12500 (Tax-free allowance)

- Dividends: £2000 (Tax-free allowance)

- Personal Savings Interest:

- £1000 (Tax-free allowance if you are a Basic Rate Taxpayer

- £500 (Tax-free allowance) if you are a Higher Rate Taxpayer

This means you could earn £12500 of general income before any tax is liable to be paid.

Could the Tax Free allowance be reduced?

The amount of Gross Income (Income before tax) you can earn before your personal allowance is reduced is based on the year you were born and how much you earn. The tax free allowance is reduced by £1 for every £2 earned over the following limits:

Year Born: Limit of earning before the tax-free allowance is reduced:

- Born after 5th April 1948 - £100,000

- Born before 6th April1948 - £30,200

This means if you were born after 6th April 1948 and earn £125000 per year, your tax-free allowance will be £0 (£25000 over £100000, divided by £2 = £12500 of personal allowance lost).

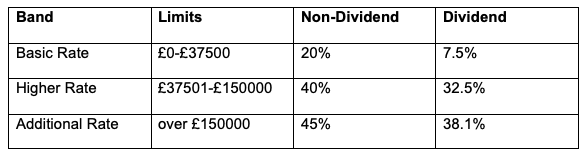

What rate of tax would you pay after the Tax-Free allowance has been applied?

The amount of income earned is taxed at a Basic Rate, then a Higher Rate and then an Additional Rate as follows:

How can you reduce the amount of income liable to the higher rates of tax?

Paying into a pension is an excellent way to increase the amount of income you can earn at Basic Rate tax. The amount you pay into a pension will increase the amount you can earn on which you pay 20% tax and you are contributing to your retirement and that amazing retirement holiday you plan to take.

How much can you earn before you pay national insurance?

National insurance is separate from income tax. You will pay national insurance on income above the thresholds between £8632 to £9500 per year based on the type of income. This means you will start to pay national insurance on income before you start to pay income tax. Rates of national insurance payable are:

- Self-employed: 9%

- Employed: £12%

- Employer: £13.8%

What are the other taxable incomes to consider?

Capital Gains Tax is tax paid on gains from the sale of an asset.

Capital Gains Annual exemption: £12300 (tax free gain)

Tax is then charged as follows:

You do not pay tax if you sell your primary home and you move.

The amount of tax-free allowance your spouse could transfer to you

If your spouse does not earn enough to use all their tax-free allowance, for example, they earn £10000 so £2500 of tax-free allowance is not being used, your spouse can not transfer the allowance to a future year for themselves but it does not have to go unused. Your spouse can transfer the allowance to you as follows:

- Transferable Marriage Allowance: £1250

Blind Person Allowance

- A blind person has an additional personal allowance £2500

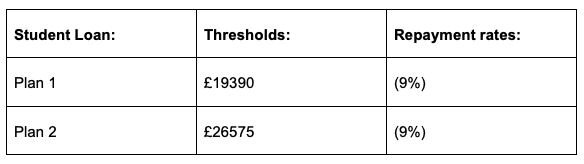

When will student loans be repayable?

Student loans are also deducted at the time the tax return is completed. Based on the student loan plan you are on, there will be a threshold amount you can earn before repaying any student loan. Once you hit the threshold relevant to your plan, you will repay the loan based on a percentage of income as follows:

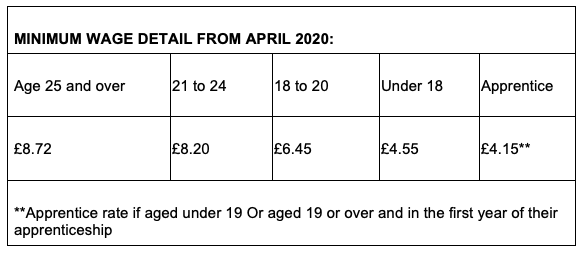

What are the minimum wage rates?

Minimum wage rates are based on age and are the minimum amounts you can pay to your staff:

Need further help with your tax calculations?

If you require any help with your tax calculations or just need some additional information, get in touch today.